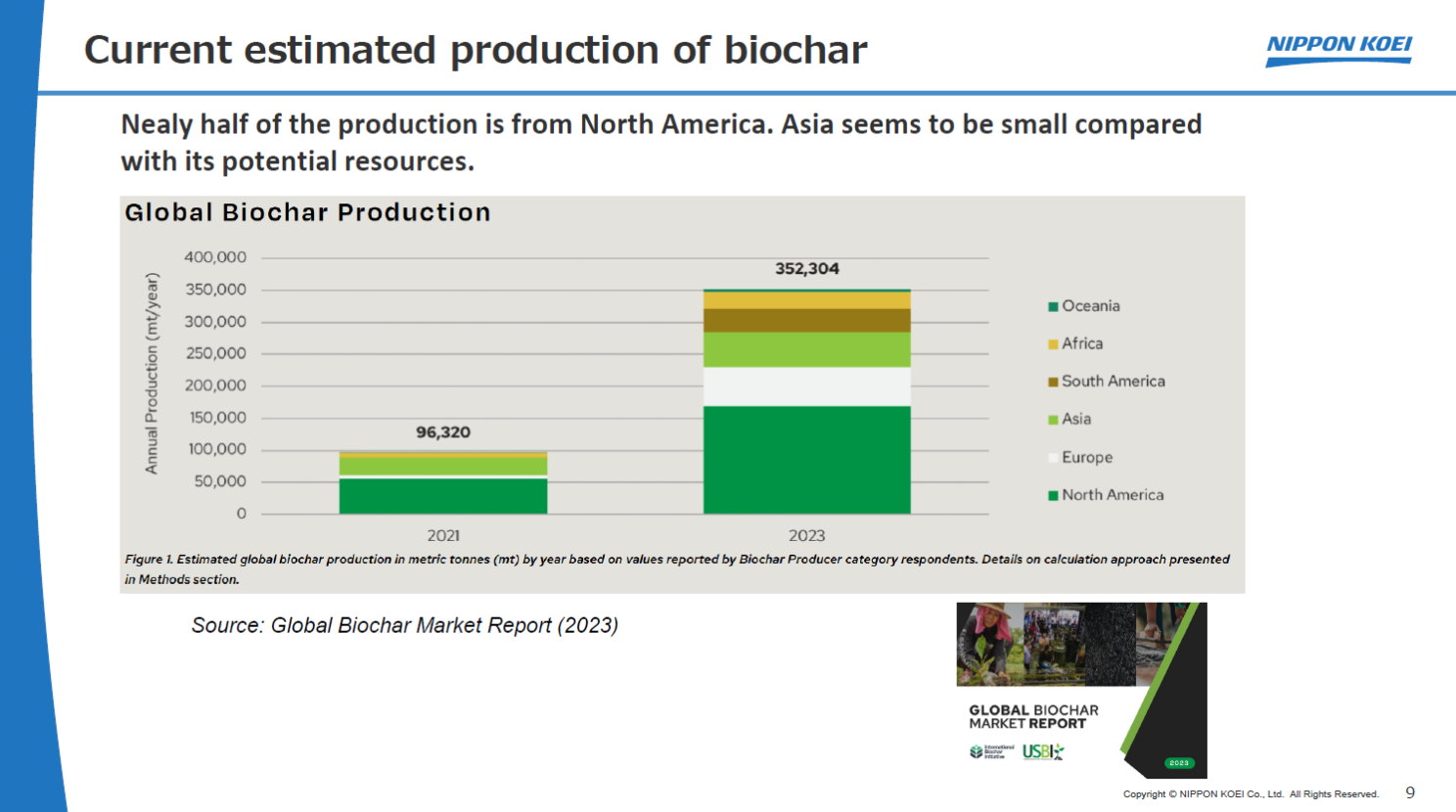

In the whirlwind of presentations at the Global Biochar Exchange in Nagoya, Japan, it was a single slide that sparked a flurry of questions. That moment came during a keynote from Mr. Tetsuya Saito of the major Japanese engineering firm, Nippon Koei. He presented a chart on global biochar production that showed a stark reality. While the vast potential for biochar feedstock lies in Asia, Africa, and Latin America, current production is overwhelmingly dominated by North America and Europe.

Screenshot of Mr. Saito’s Presentation at the Global Biochar Exchange in Nagoya, Japan in April 2025

This visible gap in production led me to wonder about the invisible structures that govern it. If the resources are in the Global South, where are the rules being written?

A quick google search into the world’s leading carbon sink registries and standards revealed a striking and uncomfortable truth: the architecture of the global carbon market is overwhelmingly headquartered in the Global North.

The fact is that many carbon offset projects are located in the Global South, but the frameworks governing their verification, and the bodies that issue the credits, are almost exclusively based in North America and Europe. The most prominent players are a testament to this geographic imbalance. Verra, which manages the world’s most widely used crediting program (VCS), is based in Washington, D.C. The Gold Standard is headquartered in Geneva, Switzerland. Puro.earth is Finnish. Other key bodies like the American Carbon Registry (ACR) and Climate Action Reserve (CAR) are rooted in the United States.

The nuance goes deeper. Even standards specifically designed for small-scale projects in developing nations often originate in the North. Mr. Saito’s own projects in Indonesia aim for credits under the “Artisan C-Sink” standard, a framework developed by the Swiss-based Ithaka Institute and Carbon Standards International. Similarly, while India’s biochar market is burgeoning, it often relies on the “Global Biochar Registry,” which is part of the European Biochar Certificate (EBC) system, again managed by European consortia.

This concentration of power raises critical questions that we, as an industry, must confront:

- Equity — If the methodologies and financial gateways are controlled from the North, how can we ensure that the economic benefits are distributed equitably along the entire value chain, especially to the local communities who are the stewards of these projects?

- Governance — Are standards developed in Geneva or Washington truly optimized for the unique agricultural, social, and economic contexts of rural Indonesia, Brazil, or Thailand? Or are we forcing a one-size-fits-all model onto a diverse world?

There are positive signs of change. Mr. Saito highlighted how Japanese initiatives are beginning to fund and develop methodologies specifically for biochar projects in the Global South. This is a crucial step toward building local capacity and more equitable partnerships.

For the global carbon market to be truly just and effective, the hands that work the soil in the South must also have a hand in writing the rules. The conversation must move beyond just where the carbon is stored, and start asking who holds the power to define its value.